SIP vs Lump Sum: Which Investment Strategy Is Better?

SIP vs Lump Sum: Which Investment Strategy Is Better?

When it comes to investing, especially in mutual funds or equities, one question often stumps investors:

Should I invest a lump sum or start a SIP (Systematic Investment Plan)?

Both strategies have their pros and cons—and the best choice depends on your financial situation, market conditions, and investment goals.

In this blog, let’s break down SIP and lump sum investing to help you decide which one suits you better.

What Is a SIP?

A Systematic Investment Plan (SIP) lets you invest a fixed amount regularly—monthly or quarterly—into mutual funds or ETFs.

It’s like a recurring deposit for the stock market, with the benefit of:

- Rupee cost averaging

- Discipline

- No need to time the market

🧾 Example:

You invest ₹5,000 every month in a mutual fund. Over a year, that’s ₹60,000—spread across different market levels.

What Is Lump Sum Investing?

Lump sum investing means putting in a large amount at once—say ₹1 lakh or more—in one go.

It works well when:

- You have idle cash (e.g., bonus, inheritance)

- The market is attractively valued or post-correction

🧾 Example:

You receive a ₹2 lakh bonus and invest it all at once in a mutual fund or index ETF.

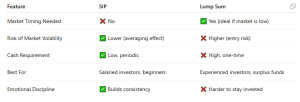

SIP vs Lump Sum: Key Comparisons

Rupee Cost Averaging: The SIP Advantage

Markets go up and down—but with SIPs, you buy more units when the market is low and fewer when it’s high.

This averages out the cost of your investments over time and reduces timing risk.

When to Choose SIP

- You have monthly income and want to build wealth gradually

- You want to avoid timing the market

- You’re just starting out and want to develop a habit of investing

✅ Ideal for long-term goals like retirement, child’s education, or wealth creation

When to Choose Lump Sum

- You have a large corpus (e.g., sale proceeds, bonus, inheritance)

- Markets are undervalued or have corrected sharply

- You’re confident about the market outlook and fund performance

📌 Pro Tip: If unsure, split your lump sum into 3–6 monthly tranches (STP) to reduce risk

Real-Life Example

Asha, 30, gets ₹3 lakh from an FD maturity. Unsure about the market, she starts a 6-month STP (Systematic Transfer Plan) from a liquid fund into an equity mutual fund.

This way, she avoids putting all ₹3 lakh in at once and benefits from rupee cost averaging.

Returns Perspective

Historically, lump sum investing gives higher returns if markets move up after you invest.

But if volatility is high, SIP may offer better risk-adjusted returns.

The longer your time horizon, the smaller the gap between the two.

❌ Common Mistakes to Avoid

- Waiting for the “perfect” time to invest a lump sum

- Skipping SIPs when the market is down

- Putting all savings into volatile assets without emergency funds

Conclusion

There’s no one-size-fits-all answer—both SIP and lump sum have their place in a smart portfolio.

- Use SIPs for regular investing and long-term wealth building

- Use lump sum when you have extra funds and the market conditions are favorable

Many seasoned investors combine both: SIP for discipline + lump sum during market dips.

Need Help Building a Strategy?

At Goodwill Wealth Management, we help you design the right investing plan—SIP, lump sum, or a smart mix—based on your risk profile and life goals.

Talk to our experts and make every rupee work harder for you.