How to Create an Emergency Fund Before You Start Investing

How to Create an Emergency Fund Before You Start Investing

Before diving into SIPs, stocks, or mutual funds, your first financial priority should be building an emergency fund. Why? Because life is unpredictable—job loss, medical bills, car repairs, or unexpected expenses can come knocking anytime.

Thank you for reading this post, don't forget to subscribe!An emergency fund acts as your financial shock absorber, allowing you to handle crises without dipping into investments or taking loans.

Let’s break down how to create an emergency fund, how much you need, and where to keep it.

What Is an Emergency Fund?

An emergency fund is a cash reserve set aside specifically to cover unexpected expenses or financial emergencies.

Examples of Emergencies:

- Job loss or salary delay

- Medical emergencies not covered by insurance

- Car or home repairs

- Sudden travel or family needs

This is not for planned expenses like vacation, new gadgets, or weddings.

How Much Emergency Fund Do You Need?

Thumb Rule:

✅ 3 to 6 months of your essential monthly expenses.

👉 If your monthly expenses = ₹30,000

✅ Emergency fund target = ₹90,000 to ₹1.8 lakh

If you’re self-employed, work in a volatile industry, or have dependents—consider aiming for 9–12 months of expenses.

How to Calculate the Right Amount

- List Essential Expenses:

- Rent/EMI

- Groceries

- Utilities

- Insurance premiums

- School fees

- Transportation

- Medical costs

2. Multiply by 3–6 months, depending on your job stability and responsibilities.

Steps to Build an Emergency Fund

✅ 1. Set a Realistic Target

Break down the target into monthly mini-goals. For example, if your goal is ₹1.2 lakh, saving ₹10,000/month gets you there in a year.

✅ 2. Create a Separate Account

Keep your emergency fund separate from your salary or spending account to avoid accidental spending.

✅ 3. Automate Savings

Set up an auto-transfer every month to a dedicated account or liquid fund.

✅ 4. Start Small, But Be Consistent

Even ₹2,000–₹5,000 per month is a great start. The key is discipline, not the amount.

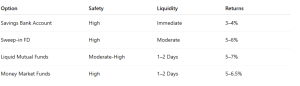

Where to Park Your Emergency Fund?

The ideal emergency fund is safe, liquid, and accessible—not volatile like stocks or locked like FDs with penalties.

🔹 Best Options:

Avoid investing your emergency fund in:

- Equity mutual funds

- Stocks

- Real estate

- Long-term FDs or ULIPs

⚠️ Mistakes to Avoid

❌ Using emergency funds for planned expenses (vacations, festivals)

❌ Keeping it all in cash (risk of theft, no returns)

❌ Not replenishing after usage

❌ Ignoring it once investments begin

Why an Emergency Fund Comes First

Without a buffer, any emergency can force you to:

- Break long-term investments (and lose compounding)

- Take high-interest personal loans or credit card debt

- Stop SIPs during tough times

✅ With an emergency fund, you stay financially stable and continue investing uninterrupted.

Conclusion

Before chasing returns, secure your financial base. An emergency fund gives you peace of mind, protects your investments, and ensures you’re prepared for life’s curveballs.

It’s not a luxury—it’s a financial essential.

🚀 Want a Personalized Emergency Plan?

At Goodwill Wealth Management, we help you set up an emergency fund, optimize where to park it, and align it with your overall financial goals.

Talk to our experts and take the first step toward smart investing—by protecting yourself first.